Discovery & lending model

Loan-as-state-machine design, role-permission matrix, e-signature flow, collections workflow taxonomy, GDPR + CCPA data-handling mapping for cross-jurisdiction readiness.

Case study · FinTech · Lending

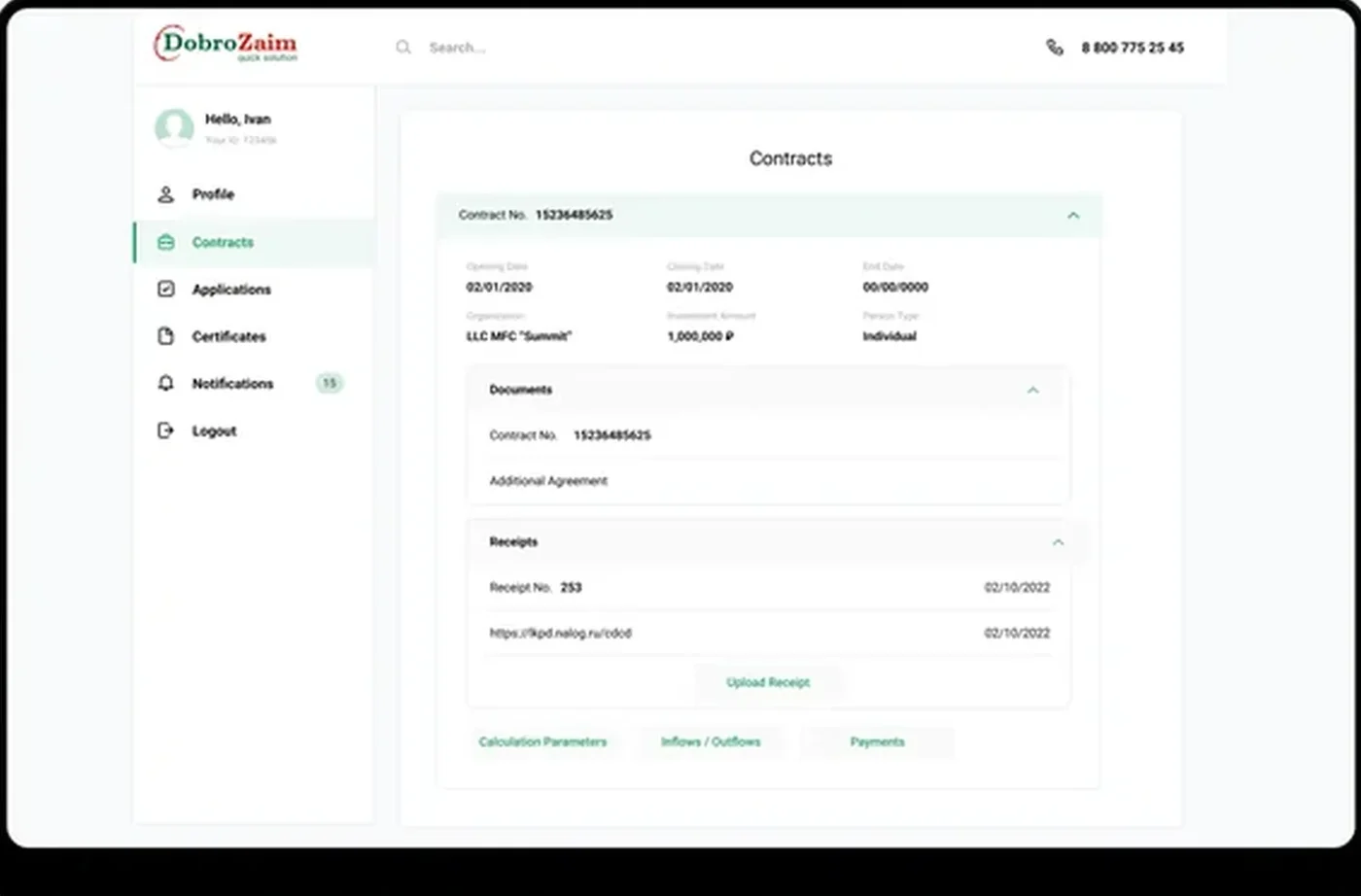

How we shipped a production microloans platform on Laravel and React — a borrower dashboard with e-signature and a repayment schedule, an underwriter workstation, a collections module, an accounting block, and a system-wide admin panel — built with audit-ready posture that translates cleanly to lending regimes across the United States and the European Union under GDPR and CCPA expectations.

The client was a microcredit operator running offline branches in a regional market and needed a digital platform to expand reach without doubling the operations headcount. The constraints were tight: a one-year delivery window, a fixed budget, and a brief that included not just the borrower-facing surface but the entire back-office — underwriting, collections, accounting, and an admin panel that the operations team could actually use. We built the platform on Laravel and React with the data model designed around the loan as a state machine, every transition logged for audit, every workspace a view over the same system of record. The result is a platform engineered for a regional launch but built with US-and-EU audit-readiness patterns so that the same codebase can support expansion into mature regulated lending regimes without an architectural rewrite.

A snapshot of what the Quick Loans Website build delivered across web, mobile, and back-office systems in its first production cycle.

A microloan operator’s software needs are not the same as a bank’s, and they are not the same as a peer-to-peer lender’s either. The product has to support the entire credit lifecycle — application intake, underwriting, e-signature, disbursement, scheduled repayment, and delinquency workflow — with each step traceable for audit and each transition reversible without losing prior state. The off-the-shelf options either targeted banks (too rigid, too expensive) or installment-payment SaaS (too consumer-facing, no underwriter workspace). We built a unified Laravel + React platform from scratch, with the data model designed around ‘loan as a state machine’ rather than ‘loan as a row in a CRM’.

The state-machine framing pays off everywhere downstream. A loan moves through draft, submitted, underwriting, approved, signed, disbursed, performing, delinquent, restructured, closed, written-off — each transition stamped with the operator, the timestamp, and the supporting evidence. The underwriter workstation, the collections module, the accounting block, and the admin panel are all views over the same state machine, which is why the same loan reads consistently across departments without daily reconciliation jobs. This is the same engineering pattern we apply across our custom software development practice when a regulated workflow has to span multiple roles in the United States and the European Union.

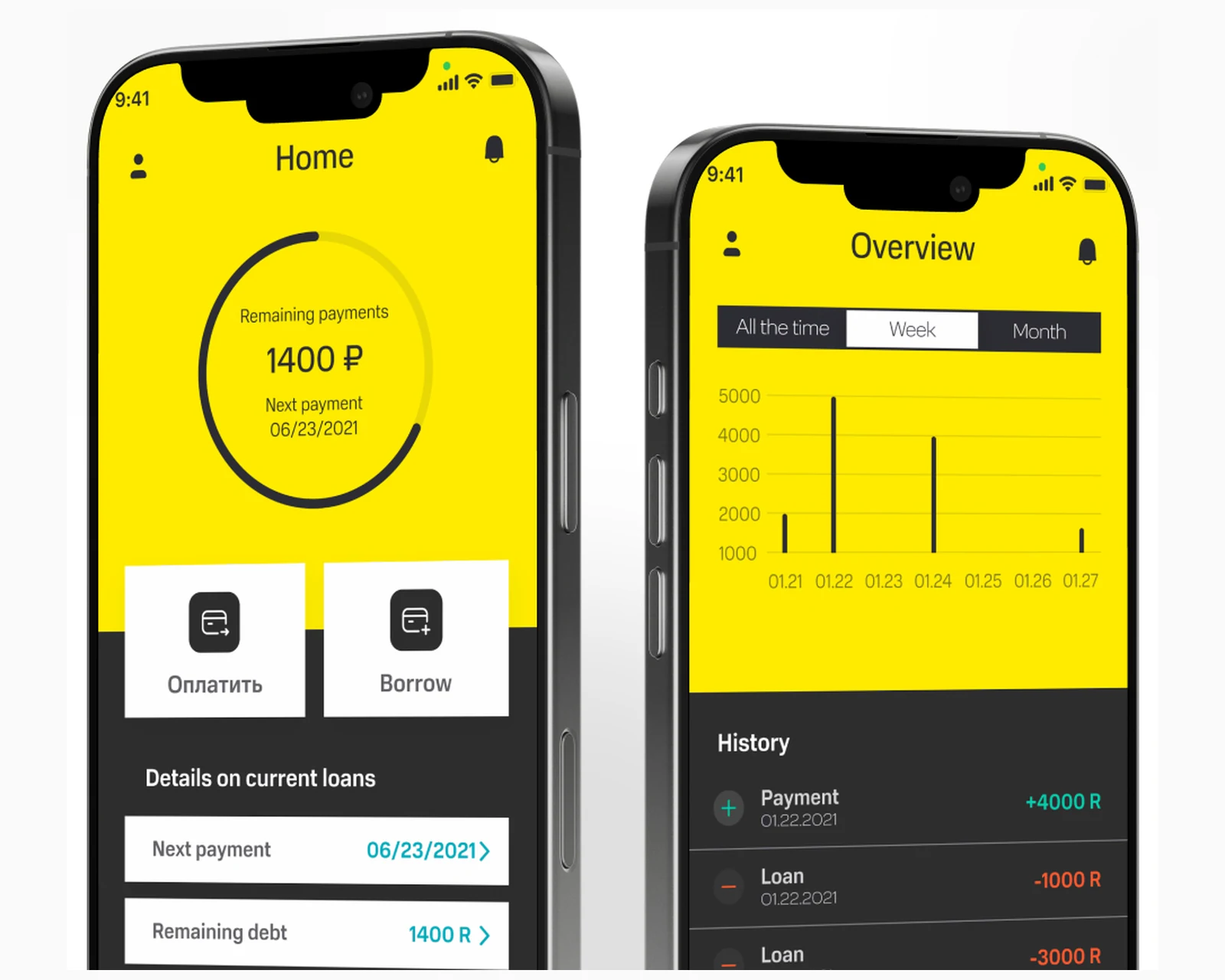

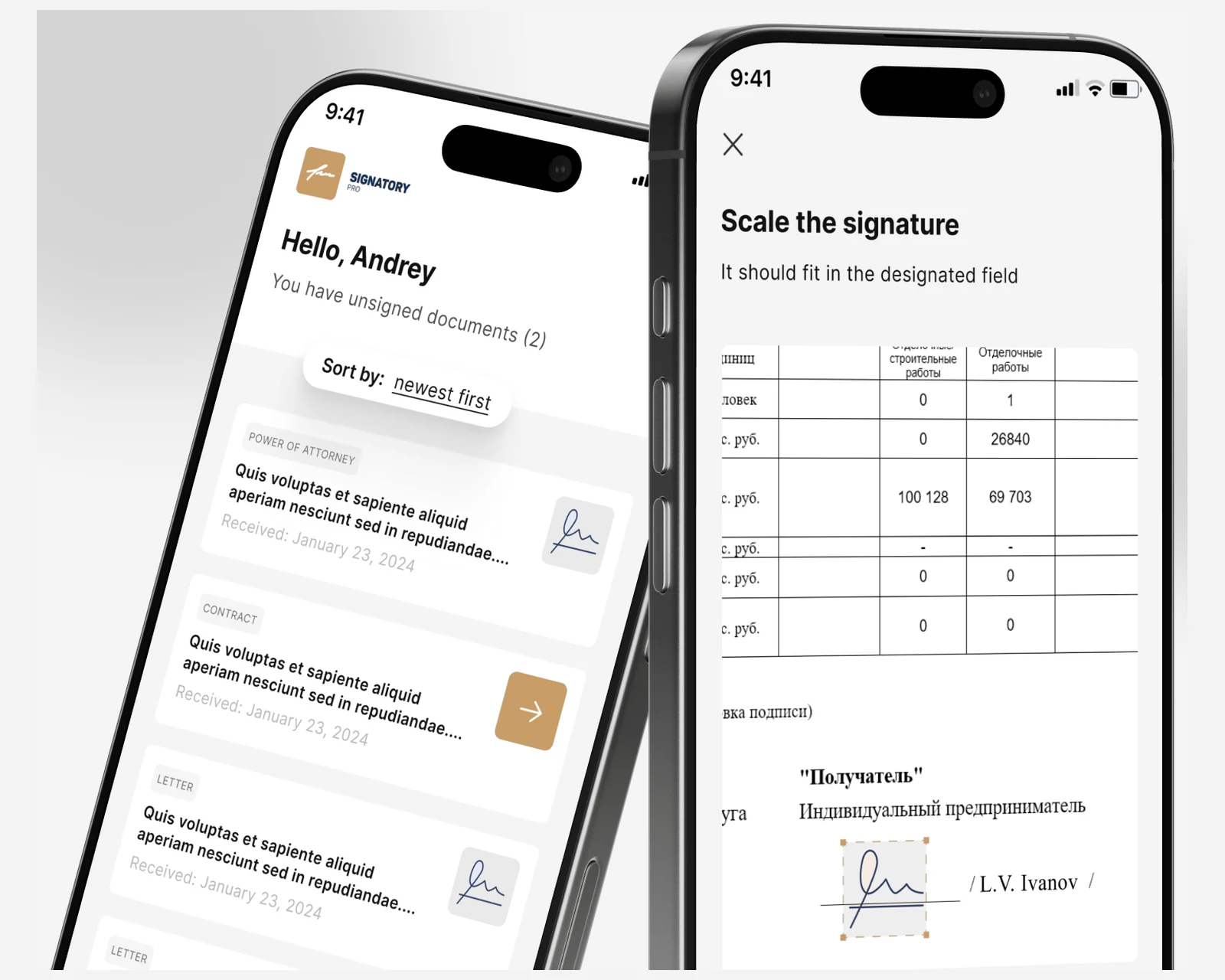

The borrower-facing dashboard is the small surface of a very deep platform. A new user signs up, fills out a streamlined application, uploads identity documents through a camera capture flow, signs the loan agreement electronically, and tracks repayment against a scheduled amortization plan — all from a responsive React frontend that runs equally well on a desktop browser at lunch and a mobile browser on the train home.

The application flow is intentionally short. A handful of fields cover identity, employment, and the requested loan amount; everything else is enriched server-side from connected data sources during the underwriting step rather than asked of the borrower upfront. The e-signature flow generates a signed PDF of the loan agreement, stores it against the loan, and emails a copy to the borrower automatically. The repayment schedule shows the next payment due, the running balance, and the total cost of the loan in a single view — no hidden fees, no rolling totals. The same pattern carries across our web application development practice when consumer-facing transparency is non-negotiable.

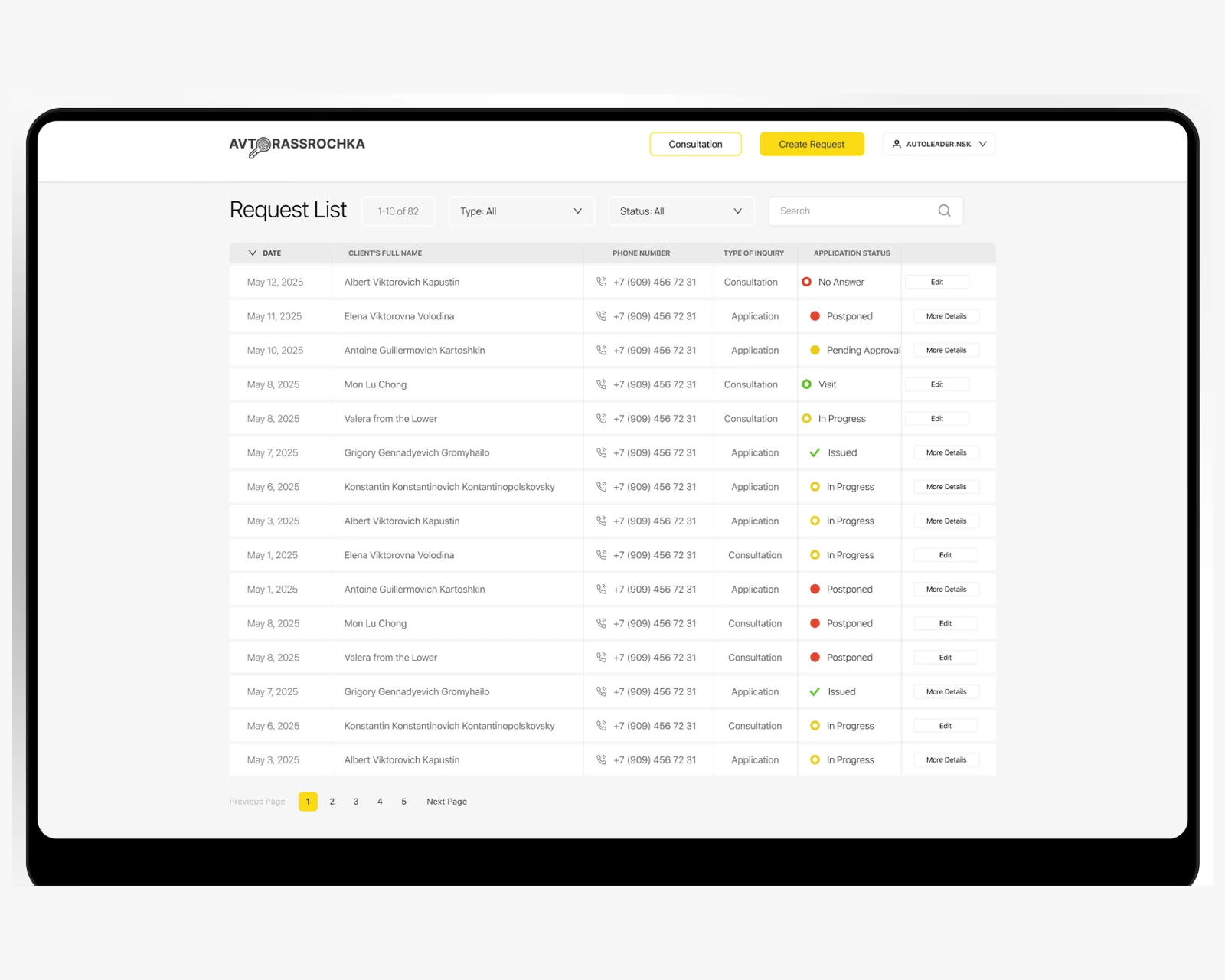

The underwriter workstation is where the platform earns its keep on the operator side. A submitted application drops into a queue, an underwriter opens it, and a single screen shows the borrower’s identity check, employment verification, credit-history snapshot, requested amount versus calculated limit, and any policy flags that fired automatically. The underwriter approves, declines, or counter-offers in one action, with a free-text rationale that becomes part of the loan’s audit trail.

The collections module handles the worst case carefully. The moment a payment misses its due date, the loan transitions to delinquent, the collections queue picks it up, and the operator works through a structured communication plan — reminder email, scheduled call, restructure offer, escalation — with every interaction logged. The accounting block sits behind both, rolling up the per-loan ledger into operator-level reports, regulator-ready exports, and a real-time view of book health.

Compliance posture is built in. Data-handling practices are aligned with GDPR obligations for users in the European Union and CCPA / CPRA obligations for users in California and the broader United States. The same patterns translate cleanly to US state lending-disclosure regimes when the platform expands beyond its original market.

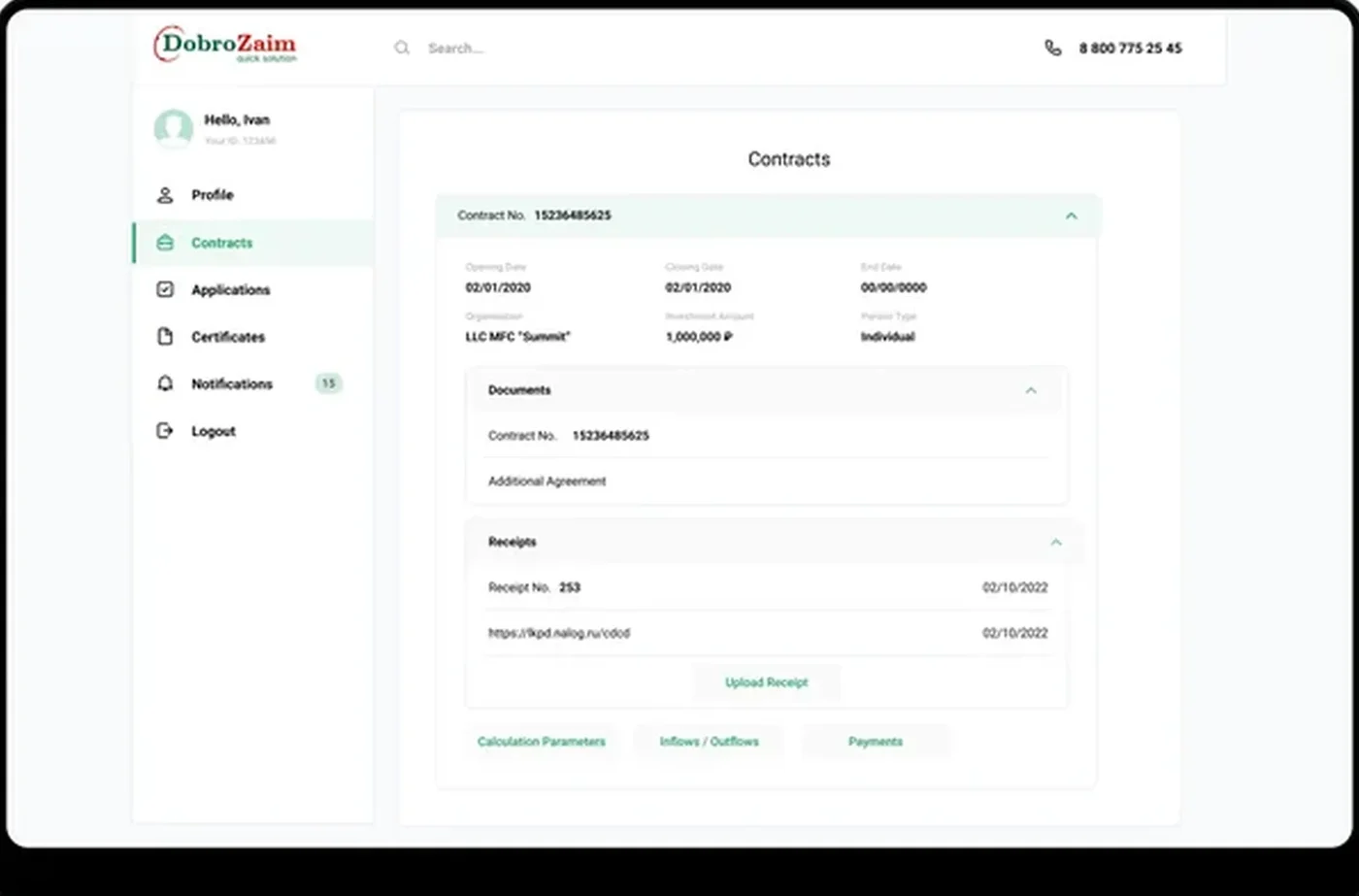

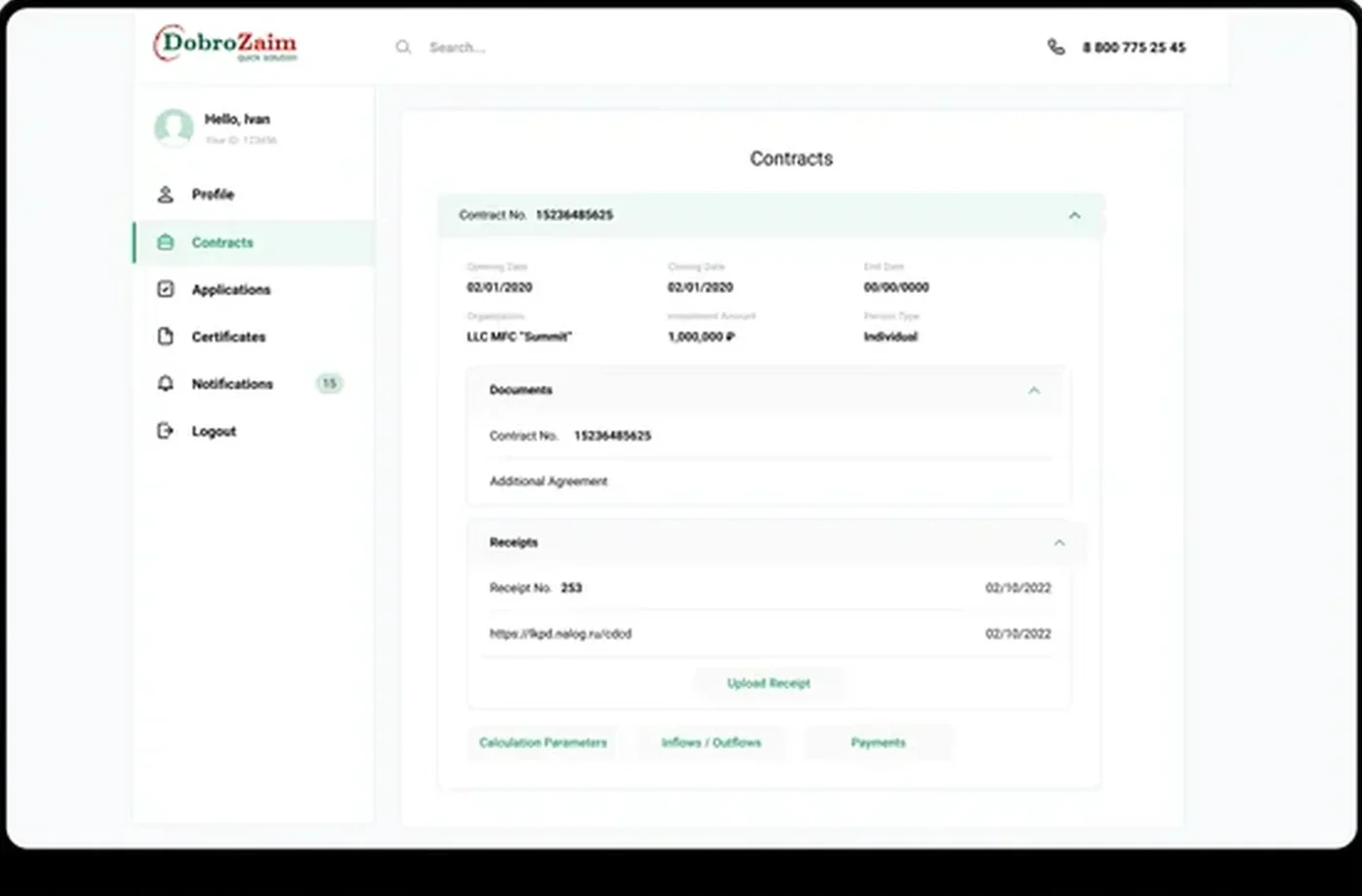

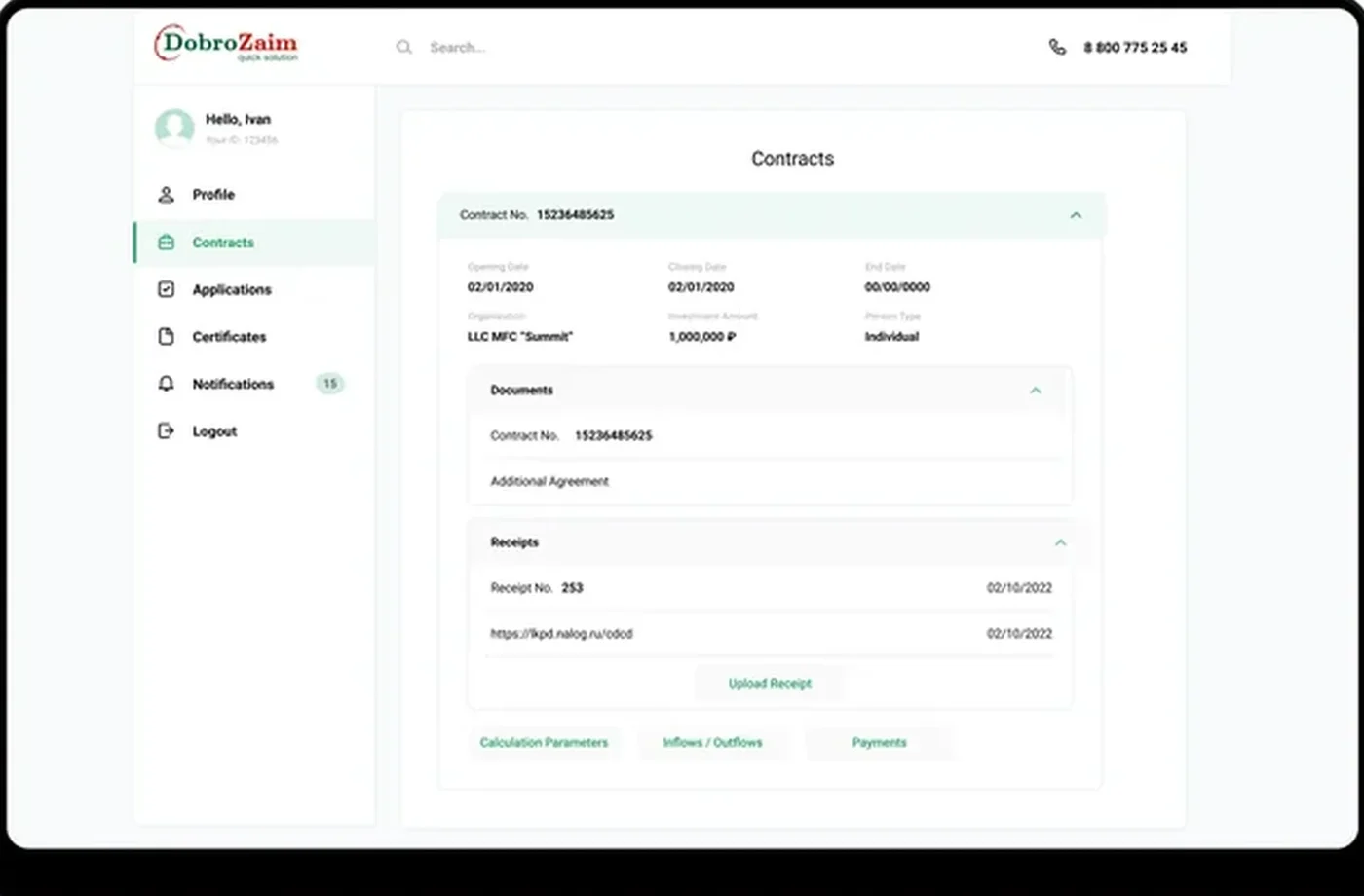

The admin panel is where the operations team configures the platform without engineering involvement: user role grants, loan-product templates with their limits and interest schedules, communication-template authoring, fee tables, and system-wide policy switches. Every configuration change is versioned and logged, which means a regulator question ‘what was your maximum loan amount on this date in this jurisdiction?’ becomes a one-query answer against the audit log.

Analytics for the operator covers the metrics that matter to a lending business: application-to-disbursement conversion rate, average ticket size, delinquency rate by cohort, recovery rate by collections strategy, and book yield net of write-offs. The dashboards run on the same PostgreSQL system of record as the rest of the platform — no warehouse drift, no nightly reconciliation needed for the operator’s daily standup.

Compliance posture: GDPR-aligned · ISO 27001 ready · SOC 2 Type II in progress · HIPAA-capable · CCPA-acknowledged.

A five-phase build that took the quick-loans platform from product specification to production across the borrower, underwriter, collections, accounting, and admin workspaces.

Loan-as-state-machine design, role-permission matrix, e-signature flow, collections workflow taxonomy, GDPR + CCPA data-handling mapping for cross-jurisdiction readiness.

Laravel API skeleton, PostgreSQL schema with append-only audit log, loan state-machine engine, configuration-versioning subsystem, regulator-export pipeline.

Five role-isolated React workspaces — borrower, underwriter, collections, accounting, admin — with shared design tokens and component primitives.

Configuration versioning enforced at the API layer, append-only audit log on every loan transition, regulator-ready export templates, third-party readiness assessment scaffolding.

Production rollout, operator-team onboarding choreography, communication-template authoring with the operations team, GDPR + CCPA compliance documentation.

Lending platforms live or die on the boring-but-critical communication layer. The platform’s communication subsystem handles automated borrower notifications — payment-due reminders, payment confirmations, delinquency notices, restructure offers — with templates the operations team authors in the admin panel rather than the engineering team coding them into a release. The template engine supports variable substitution, multi-language tracks, and channel routing (email, SMS, in-platform inbox), and every message sent is logged against the loan for audit. Restructure flows are first-class: when a borrower can’t make a scheduled payment, the operator can offer a restructured schedule from the collections module, the borrower accepts it through the same e-signature flow as the original loan, and the loan’s state machine records the restructure as a discrete event without losing the prior payment history. The whole subsystem was built with extensibility in mind: adding a new loan product, a new communication channel, a new restructure variant, or a new regulator export template is a configuration change against the admin panel, not a code release. This pattern translates cleanly to our cloud & DevOps practice when an operations team needs to ship changes without an engineering deploy.

The platform launched in its original regional market on schedule and within the approved budget, with a system architecture engineered to translate cleanly into the United States and the European Union if the operator chooses to expand. The borrower-facing surface uses US-and-EU UX patterns — transparent total-cost disclosures, no hidden fees, clear consent flows for any optional analytics — that map onto Truth-in-Lending-style disclosures in the US and onto consumer-credit disclosure rules in the EU. Data-handling practices are aligned with GDPR for any future European users and with the US state-privacy patchwork — CCPA / CPRA (California), VCDPA (Virginia), CPA (Colorado), CTDPA (Connecticut), UCPA (Utah), TDPSA (Texas), and Oregon CPA. The same patterns translate to state-level lending licensure regimes — California Financing Law, New York DFS licensure, Texas OCCC licensure — without an architectural rewrite, because the configuration layer was built for multi-jurisdiction support from day one.

Infrastructure-wise, the platform was deployed on a single regional cluster at launch but architected to split cleanly across EU and US data centers when the operator scales beyond its original market — the Netherlands, Germany, France, Sweden, and Ireland for EU coverage; US East and US West for North America. The system-of-record PostgreSQL instance can be split per-jurisdiction for data-residency commitments without changing the application layer. The in-platform privacy policy was drafted to document the architecture above, citing GDPR obligations and California CCPA obligations directly. The engineering team behind the build sits across CET and runs a CET workday with East-Coast US overlap (9 AM–1 PM ET) for stand-ups, regulator-question turnaround, and incident response — the timezone window that lets a US product team and an EU engineering team share four hours of live overlap every day.

The active custom software development roadmap for the platform includes a native mobile companion app for the borrower workspace, an automated underwriting tier with rules-engine policy authoring (replacing some manual underwriter touches on the lowest-risk applications), expanded regulator-export templates for additional jurisdictions, and a multi-product engine that lets a single operator run installment loans, lines of credit, and salary-advance products on the same platform. A deeper analytics layer is planned for portfolio risk modeling — cohort delinquency curves, predicted-loss reserving, recovery-strategy A/B tests — with the system-of-record schema already structured to support per-loan event sourcing. Infrastructure plans include further automation under the cloud & DevOps roadmap.

If you are planning a microloans platform, a consumer-credit product, or any FinTech build where the loan lifecycle has to be auditable, configurable, and multi-workspace from day one for audiences in the US and EU, we have shipped this stack end to end and can compress the build timeline meaningfully. The reference build is documented at case reference, and the engineering team behind it sits inside YuSMP Group. We work fixed-price for well-scoped MVPs and on dedicated development teams for ongoing delivery, with a CET workday and a guaranteed East-Coast US overlap (9 AM–1 PM ET) window for stand-ups, demos, and incident response.

A focused lending-platform MVP covering a borrower dashboard, an underwriter workstation, a basic collections module, an accounting block, and an admin panel typically costs $140k–$320k. Adding multi-product support, an automated underwriting tier, regulator-export templates for multiple jurisdictions, a mobile borrower app, and a hardened audit-log subsystem brings a full-featured product to $380k–$780k. The dominant cost drivers are the loan-as-state-machine design, the multi-workspace permission model, and the configuration-versioning subsystem that lets the operations team ship policy changes without engineering involvement.

Off-the-shelf banking cores are built for banks: they assume regulator-bound balance-sheet products, multi-currency ledgers, and integration surfaces that microloan operators do not need and cannot afford to license. Laravel gives you a mature PHP framework with a strong job-queue system, an authentication layer that maps cleanly onto role-isolated workspaces, and a community-tested ecosystem. React on the frontend lets you ship five role-scoped workspaces from a single codebase with shared component primitives. The Laravel API plus React SPA pattern keeps the engineering boundary clean and the time-to-market under a year for a focused MVP.

Audit-readiness is an architecture decision, not a documentation exercise bolted on at the end. Every loan transition writes an append-only event to the audit log with the operator, the timestamp, and the supporting evidence. Every configuration change in the admin panel is versioned so a regulator question ‘what was your maximum loan amount on this date in this jurisdiction?’ becomes a one-query answer. Every borrower interaction, every underwriter decision, every collections communication is logged against the loan for the lifetime of the platform. The same posture maps cleanly onto GDPR data-subject-access requests, CCPA right-to-know requests, and US-state lending-disclosure regimes.

The moment a payment misses its due date, the loan transitions to delinquent in the state machine, and the collections module picks it up into a structured queue. The collections operator works through a configurable communication plan — reminder email, scheduled call, restructure offer, escalation to legal — with every interaction logged. Restructure flows are first-class: a renegotiated schedule is a discrete event on the loan, not a destructive overwrite of the original schedule, which means the platform retains the full payment history for audit even when the schedule changes mid-flight.

A focused MVP covering a borrower dashboard, an underwriter workstation, a basic collections module, an accounting block, and an admin panel typically takes 28–40 weeks. Adding multi-product support, an automated underwriting tier, expanded regulator-export templates, and a native mobile borrower app adds 12–18 weeks. The audit-ready hardening pass — append-only audit log, configuration versioning, third-party readiness assessment — is frequently underestimated and should be budgeted at 4–6 weeks of dedicated work.

Related cases

Dealer-financing platform with installment plans, audit-ready workflows, multi-role workspaces.

View case →

Cross-platform e-signature product — audit-ready posture, US + EU launch, GDPR + CCPA-aligned.

View case →

Unified crypto-ecosystem hub aggregating multiple tokens — live exchange data, charts, direct purchase.

View case →Share a few details and a senior consultant will reply within one business day.